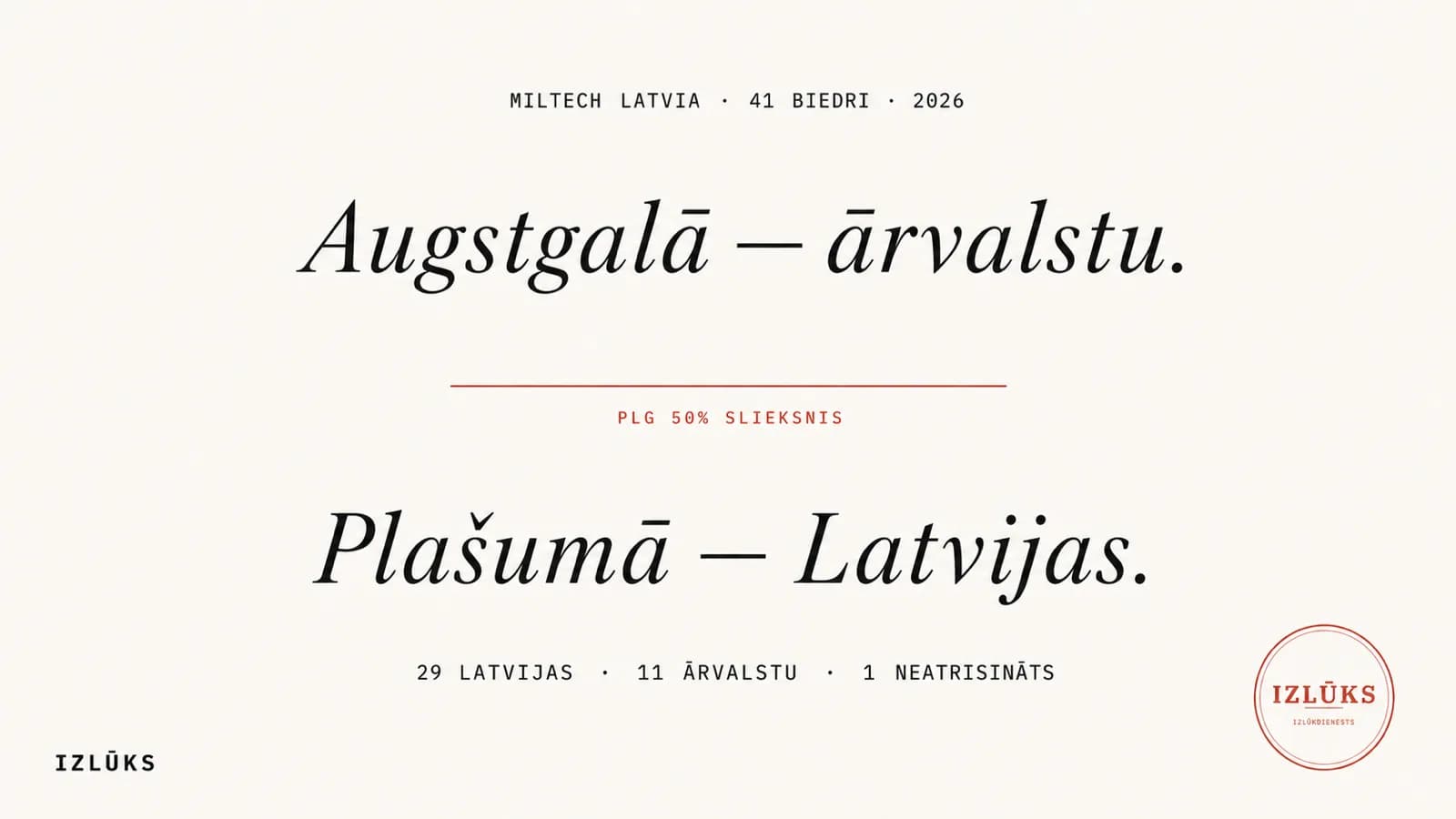

MilTech Latvia gathers 41 regular members — from LMT Defence and Redwire down to ten-person workshops. Ranked by defence-attributable revenue, foreign owners hold roughly three-quarters of the top ten. What belongs to Latvian owners is the breadth of the list — many members below the top.

The previous issue looked at how EU money to Latvia has changed colour — the defence share rising from zero to roughly a quarter. Now: where this money lands.

Ranking by group revenue would mislead. Most Latvian defence-industry companies are not defence-only companies. LMT reported €333.8M in revenue in 2025 — but the defence segment is a 140+ engineer slice whose annual line we estimate in the €15–30M band.1 EMJ Metāls group revenue is €26.2M, but the Patria 6×6 hull production line is only one part of a metalworking book we estimate at €4–7M.2 Axon Cable in Daugavpils reported €40.7M — but the defence segment is roughly 35%, or about €14M.3

So this ranking does not use group revenue. It uses defence-attributable revenue — the share of revenue that follows from defence and security customers. For pure-play defence firms (Origin Robotics, Brasa Defence Systems, Eraser) it effectively equals the annual report line. For diversified groups we provide a range and a cited evidence base, not a single point estimate.

The second filter is ownership. The previous article stopped at the direct-shareholder level: if an SIA is owned by another Latvian SIA, we classified it as Latvian. This ranking goes one step further and follows the ownership chain to the ultimate beneficial owners (UBOs). Latvian-owned means strictly that more than 50% of UBO equity is held by Latvian natural persons or the Latvian state. Everything else is foreign.

This stricter filter changes the classification of at least one SIA. Ardlat is directly owned by SIA Ardelta — a Latvian SIA — but Ardelta's sole shareholder and UBO is Aaron Timothy David McElroy, an Irish national resident in France. The previous article classified this SIA as Latvian; the UBO rule reclassifies it as foreign. That is where the threshold sits: what the press calls "a Latvian family office" is, in the register, an Irish UBO.

First view — the full list

The top ten by defence-attributable revenue:

| # | Company | Defence rev. (€) | Reporting year | Owner |

|---|---|---|---|---|

| 1 | Redwire Defense Tech Riga | 68.3M | 2024 | foreign (US) |

| 2 | LMT Defence (segment) | 15–30M | 2025 | Latvian state (51%) |

| 3 | Axon Cable in Daugavpils | ~14M | 2025 | foreign (France) |

| 4 | Brasa Defence Systems | 11.00M | 2024 | Latvian |

| 5 | Ammunity | 7.66M | 2025 | foreign (Sweden, since Nov 2025) |

| 6 | Eraser | 6.00M | 2025 | Latvian |

| 7 | ISP Optics Latvia (LightPath) | 5.3–7.4M | 2024 | foreign (US) |

| 8 | EMJ Metāls (segment) | 4–7M | 2024 | foreign (US) |

| 9 | Atlas Aerospace | 3.52M | 2024 | foreign (Israel, since Nov 2025) |

| 10 | Victec | 3.27M | 2025 | Latvian |

In the top ten, six of the ten defence lines are foreign-owned and control roughly €105M out of the top-ten total of ~€143M — about 74%. Latvian private ownership — Brasa, Eraser, Victec — controls ~€20M (14%); the central estimate for the LMT state segment is ~€17.5M (12%). An eighth of the top of Latvia's defence industry belongs to Latvian private capital.

The remaining 31 members split as follows: one company (Origin Robotics) above €1M; six in the €0.3–1.0M band; eight in the €0.05–0.3M band; five with first-year revenue below €50k; ten with zero or no filed annual report yet; and one — Marta — that remains unresolved because no legal entity in the register matches this MilTech logo. The full ranking and each company's calculation are available in the research materials accompanying this article.

Second view — Latvian owners only

This is the interesting list. After the UBO filter, 29 members remain in Latvian hands. The top ten:

| # | Company | Defence rev. (€) | Reporting year | Notes |

|---|---|---|---|---|

| 1 | LMT Defence | 15–30M | 2025 | Latvian state holds 51% of LMT shares |

| 2 | Brasa Defence Systems | 11.00M | 2024 | NBS uniform production (LATPAT); roughly 16 NATO and partner armies as customers |

| 3 | Eraser | 6.00M | 2025 | From €42k to €6.00M in a single year — a 143× increase |

| 4 | Victec | 3.27M | 2025 | Stealth USVs and UAVs; NATO manufacturer certification and AQAP-2110 |

| 5 | Origin Robotics | 1.81M | 2024 | A rare Latvian EDF coordinator (MPortISTAR) |

| 6 | DK Unity | 0.92M (trough year) | 2024 | Pastnieks FPV — NATO catalogue, three MoD customers |

| 7 | Perkons Energy | 0.2–0.9M | 2025 | Battery packs for drones; same founders as DK Unity |

| 8 | Elektroniskie sakari | 0.2–1.0M | 2024 | State spectrum regulator with NBS radio-monitoring product lines |

| 9 | Temeso | 0.37M | 2025 | NBS aerial-target platforms — Ministry of Defence named the company in a market-research notice |

| 10 | Baltic Bullets | 0.14–0.33M | 2024 | Specialty rifle projectiles (.308, .338, .50 BMG); 15× tax-payment run-rate Q1 2026 |

The Latvian top five — LMT Defence, Brasa, Eraser, Victec, Origin Robotics — together account for roughly €37–55M of defence revenue (depending on the central LMT segment estimate). That is less than Redwire alone (€68.3M).

Below the €1M line, Latvian ownership continues across another 24 members — UGV, UAV, sensor, optics, equipment, battery, ammunition and metalworking firms that have not yet reached production scale but have a name in the register, an annual report or a first tax line. Among them: companies the Ministry of Defence has named in market-research notices (Temeso), holders of Latvian Armed Forces contracts (VR Cars FOX, Natrix UGV), and one specialty gimbal IP line that did not transfer with Edge Autonomy's 2021 acquisition (Gorgon Optronics).

This breadth has structural significance. Scale comes and goes with ownership transactions: in June 2025 Edge Autonomy moved to a US-listed parent (Redwire Corporation); in November Atlas Aerospace moved to Israel's Xtend; in early November Ammunity moved to Sweden's Astor group. There is no transaction in the other direction — no Latvian company acquiring a foreign defence firm. That gradually makes the top of Latvia's industry more foreign, while the middle tier remains predominantly Latvian.

Third view — what the UBO rule changes

The previous article worked with a direct-shareholder classifier. This ranking moves to the ultimate-beneficial-owner threshold test. In practice it changes four things.

Ardlat is owned by SIA Ardelta. At the direct level — Latvian. At the UBO level — an Irish citizen. Classification flips to foreign.

LMT Defence is a segment of LMT. Through Possessor, LVRTV and Tet equity stakes the Latvian state controls 51%; the UBO rule classifies it as Latvian. But the Telia minority (49%) sits with a Swedish parent — if it ever calls its share of accumulated profit, a single decision's outflow from Latvia will exceed everything observed to date.

NEWT21 (22% Ukrainian co-founder) and Beyron (24% Ukrainian co-founder) remain Latvian — above the 50% threshold of Latvian natural persons. Ukrainian minorities in Latvian defence-tech newcos after 2022 are a qualitatively separate article in their own right.

Marta — a logo on the MilTech regular-member roster, but no identifiable legal entity in the register. The logo exists; the company with this name we do not see. In the list it remains unassigned.

The largest defence-industry company in Latvia remains foreign-owned. The largest Latvian-owned one is the state. The rest — many, small, not yet at scale.

Notes

Footnotes

-

LMT (Latvijas Mobilais Telefons) ownership structure: Sonera Holding B.V. 24.5% + Telia Company AB 24.5% (total 49% Telia group); Tet 23% + Latvian State Radio and Television Centre 23% + Possessor 5% (total 51% Latvian state). 2025 annual report: revenue €333.8M, net profit €33.4M, dividends paid €0. The €15–30M defence-segment estimate used in this ranking is triangulated from the engineering team size (140+ engineers and developers), active EDF contract values and publicly announced MoD/NAF work. LMT does not separately publish a defence-segment P&L. ↩

-

SIA EMJ Metāls (reg. 40103316638), 2024 annual report: €26.17M revenue, 141 employees; core business is a generalist sheet-metal service centre with more than 1,000 customers per year across Nordic, DACH and Baltic markets. 100% owned by AMARI Metall Nordosteuropa GmbH (Germany) since June 2023; UBOs are three members of the Colburn family (US citizens, US residents). The €4–7M defence-segment estimate is triangulated from Patria's publicly named four Latvian suppliers (Defence Partnership Latvia, SFM Latvia, EMJ Metāls, Metāro), the Valmiera assembly line's throughput (~30 6×6 vehicles per year × €1.0–1.2M each) and EMJ's share of headcount on the military line (roughly 30–50 of 141). Certification for independent welding of 6×6 hulls was issued in December 2023; the first locally assembled Patria 6×6 was handed over to the Latvian Armed Forces in August 2024. Sources: SIA EMJ Metāls 2024 annual report via Latvian Enterprise Register open data; Patria group communications on cooperation with Latvian suppliers; Latvian Ministry of Defence statements on the CAVS programme and the 56-vehicle command-variant add-on (2024-11-14). ↩

-

SIA Axon Cable (Daugavpils, reg. 41503025401), 2025 annual report: €40.73M revenue, 643 employees, +13.2% YoY. 100% owned by Axon' Cable S.A.S. (France, Montmirail), a family-owned business; UBO is Joseph Puzo (French national, French resident). The Daugavpils plant produces high-tech cable harnesses, connectors, plastic-moulded interconnect components and interference-protection assemblies for aerospace, defence, space, medical and automotive customers; it built the harnesses for all 650 OneWeb satellites. At group level, aerospace + defence accounts for roughly 50% of the portfolio, space and medical for ~10% each, and the remainder for automotive and industrial. The Latvian plant's defence-segment estimate of

35% (€14M, range €8–20M) is derived by applying the group portfolio share to Daugavpils output. No separate Latvia-level segment breakdown is published. Sources: SIA Axon Cable 2025 annual report via Latvian Enterprise Register open data; Axon' Cable group public communication on customer portfolio; LIAA Latvian Tech in Space directory; Office of the President of Latvia statement on the inauguration of the new Daugavpils plant (2022-04-05). ↩